Figure 1. Provides an overview of transferring the risk/return securitization instruments.

This article provides a review of the securitization instruments in the context of the subprime mortgage crisis of 2008. The decreasing housing prices in the u. 8. Caused the increasing mortgage defaults and the increasing mortgage defaults caused this subprime mortgage crisis and this crisis is exploded by securitization instruments (e. G., CDS] which are just too complex to see their risks. This article will provide a specific classification of securitization instruments and distinguishes between two main classes of securitization instruments.

The first classes are mortgage-backed security [MBS], asset-backed security [ABS], asset-backed commercial paper [ABCP] and cash-flow collateralized debt obligation [CDO]. The second category of securitization instruments includes credit default swap (CD8) and synthetic collateralized debt obligation [synthetic CDO). Finally, this article ends with a short discussion of the roles of the Credit Rating Agency(CRA) in the financial crisis.

To follow the analysis below, the reader should note the following terminology. Subprime mortgage securitization. The type of securitization whose failure initially triggered The chain of failures that became the subprime- Mortgage financial crisis (hereinafter the "subprime Crisis"), is a subset of mortgage securitization. In the most Basic form of mortgage securitization, mortgage—backed Securities ["MBS") are issued by a special-purpose vehicle ("sp "). More complex forms of mortgage-backed Securities include collateralized debt obligation ("CDO"). Credit default swap (CDS), synthetic CDO, and ABS CDO. Throughout this article, CDS, ABS, MBS, ABCP: CDO and CRA Will refer to both the singular and plural form.

When homeowners default, the payments received by MBS investors decline and the perceived credit risk rises. This has had a significant adverse effect on investors and the entire mortgage industry. Those subprime defaults caused this mortgage crisis of 2008. This crisis caused a Chain reaction throughout the global financial markets And the banking system, because the NPV of investments Related to housing prices decreased greatly, putting the Main financial institutions at a serious disadvantage.

Because all financial institutions tightened their lending Practices, all personal and all corporate capital spending decreased. This crisis is rooted in about 1997, but is more evident in about 2008. This crisis has passed through various stages. This crisis is revealing universal weaknesses in the global financial system and supervisory structure. Across the globe, all assets prices decreased, volatility Levels increased, credit spreads increased greatly and Liquidity demand increased greatly. Uncertainty is Unusually clear in the asset—backed commercial paper (ABCP] market. All financial institutions around the world Have reported losses of approximately U.S. $435 billion as Of 17 July 2008. Those cause central banks around the World to invest in a large number of cash into their financial markets. The central banks encourage lending to worthy borrowers and to regain faith in the ABCP markets. The U.S. Government also bailed out key financial institutions to Undertake significant additional financial promises.

This article proceeds as follows. Section t provides an Overview of securitization and discusses its specific characteristics. Section 2 provides an overview of CDS Securitization and discusses its specific characteristics. Section 3 presents a detailed development of the subprime mortgage crisis. Section 4 concludes and Analyses the main channels through which securitization Instruments contributed to the initiation and propagation Of the subprime mortgage crisis.

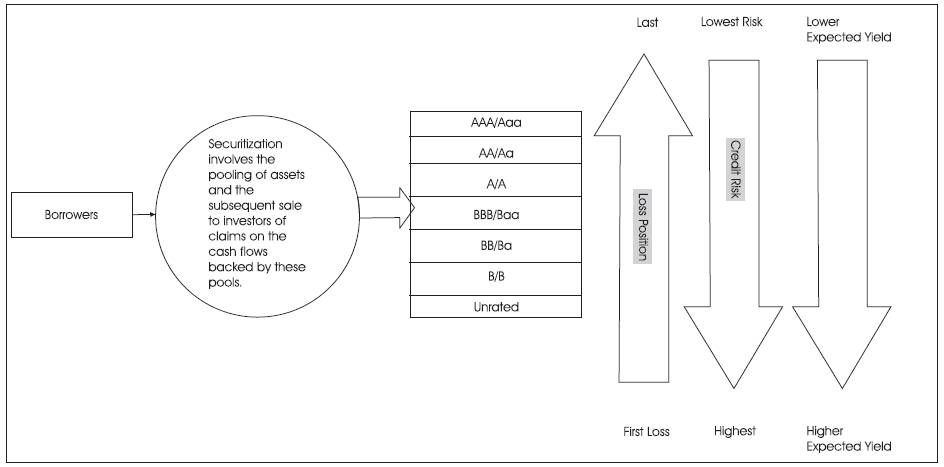

All assets can be securitized so long as they are associated with cash flow. Securitization is a broad term used to describe a sector of finance that was created to help transfer risk using complex legal and corporate entities. Securitization is the repackaging of cash flows that can transform the risk, return and liquidity characteristics of financial portfolios. Figure 1 provides an overview of transferring the risk/return securitization instruments. Securitization involves the pooling of assets and the subsequent sale to investors of claims on the cash flows backed by these pools.

Figure 1. Provides an overview of transferring the risk/return securitization instruments.

Typically, several classes [or tranches] of securities are issued, each with distinct risk-return profiles. The word tranche is French for slice, section, series, or portion. The tranching is an important concept in securitization because it is the system used to create different investment classes for the securities that are created in the securitization world. The tranching allows the cash flow from the underlying asset to be diverted to the various investor groups. The tranching of these securities into instruments with different risk/return profiles facilitates marketing of the bonds to investors with different risk appetites and investing time horizons. A suitably large portfolio of assets is "pooled" and sold to a "special purpose vehicle" or "SPV" (the issuer) a tax-exempt company or trust formed for the specific purpose of funding the assets. Once the assets are transferred to the issuer, there is normally no recourse to the originator. The issuer is "bankruptcy remote," meaning that if the originator goes into bankruptcy, the assets of the issuer will not be distributed to the creditors of the originator. To be able to buy the assets from the originator, the issuer SPV issues tradable securities to fund the purchase. Investors purchase the securities, either through a private offering (targeting institutional investors] or on the open market. The issuer [SPV] within a corporate group (American International Group (AIG)) is said to be bankruptcy remote when the insolvency of that SPV does not affect any other company in the group (AIG), particularly any holding company or subsidiary company of the bankruptcy remote vehicle. If the SPV goes into bankruptcy, no other company in the same group (AIG) would be affected. In addition, the credit risk of the collateral asset pool is separated from the credit risk of the originator, through the Involvement of a special purpose vehicle (SPV) or special Purpose entity (SPE). The special purpose legal vehicle r 3 (typically a trust incorporated in the Cayman Islands] that Will purchase the assets and issue the CDO's tranches. The Principal and the interest of the MBS issued by the SPV Depend on the cash-flows produced by the pool of Underlying financial assets (such as residential Mortgages). The SPV sell these tranches of securities to investors in the capital markets. The originator initially owns The assets engaged in the deal. This is typically a Company looking to raise capital, restructure debt or Otherwise adjust its finances. Under traditional corporate Finance concepts, such a company would have three Options to raise new capital: a loan, bond issue, or issuance of stock. Once the assets are transferred to the Issuer, there is normally no recourse to the originator.

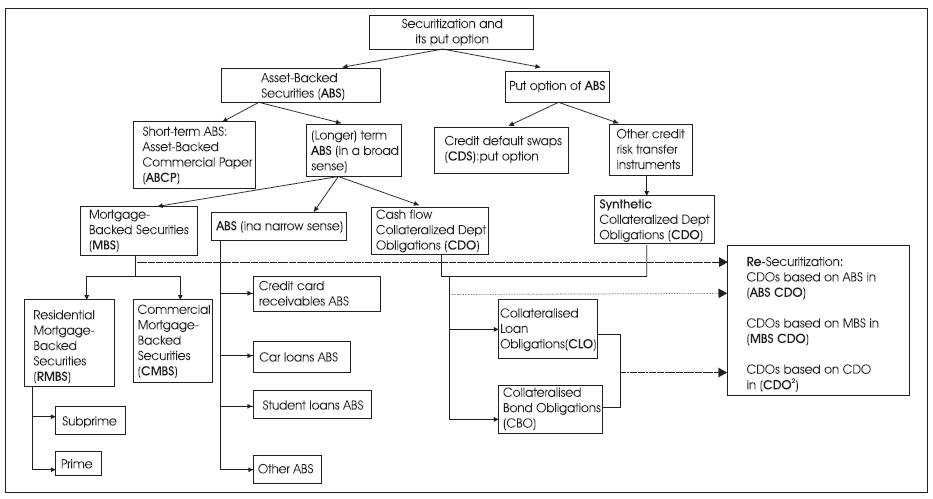

As has become clear from the introduction above, Securitization is strongly interrelated with securitization. Securitization, in a narrow sense, is used almost interchangeably with securitization. In different words, Securitization can also be interpreted as a financing mechanism, or a process in which assets are refinanced In the capital markets by issuing securities sold to investors By a SPV. Figure 2 provides an overview of the main Securitization instruments.

Figure 2 provides an overview of the main securitization instruments.

Securitization is a securitization process, which involves Pooling and repackaging of cash flow producing Financial assets into securities that are then sold to investors. The name "securitization" is derived from the fact That the form of financial instruments used to obtain funds from the investors is securities. As a portfolio risk backed by Amortizing cash flows [and unlike general corporate debt) The credit quality of securitized debt is no stationary due to Changes in volatility that are time-dependent and Structure-dependent. If the transaction is properly Structured and the pool performs as expected, the credit Risk of all tranches of structured debt improves; if Improperly structured, the affected tranches will Experience dramatic credit deterioration and loss.

Securitization is the process through which an issuer Creates a financial instrument by combining other Financial assets and then marketing different tiers of the repackaged instruments to investors. The process can Encompass any type of financial asset and promotes liquidity in the marketplace. The process creates liquidity by enabling smaller investors to purchase shares in a larger asset pool. Using the MBS example, individual retail Investors are able to purchase portions of a mortgage as a type of bond. Without the securitization of mortgages, Retail investors may not be able to afford to buy into a Large pool of mortgages.

The following will explain the securitizations, which have played the most prominent roles in the subprime mortgage crisis of 2008. There are four types of securitizations: ABS, MBS, ABCP and CDO.

In finance, an ABS is a type of debt security that is based on pools of assets, or collateralized by the cash flows from a specified pool of underlying assets. Securitization makes these assets available for investment to a broader set of investors. These asset pools can be made of any type of receivable from the common, like credit card payments, auto loans, student loans, and mortgages, to deep cash flows such as aircraft leases, royalty payments and movie revenues. Representatively, the securitized assets might be highly illiquid and private in nature.

A significant advantage of ABS is that they bring together a pool of financial assets that otherwise could not easily be traded in their existing form. By pooling together a large portfolio of these illiquid assets they can be converted into instruments that may be offered and sold freely in the capital markets. ABS enables the originators of the loans to enjoy most of the benefits of lending money with bearing little the risks involved. ABS is generated through a securitization process by SPE (SPV) in order to transform illiquid assets of the originator into transferable securities. The SPV is designed to separate investors from the credit risk of the originating financial institution. SPV (SIV] issue and sell the ABS to investors. This allows for the issuing institution to be legally separated from the SPV.

The underlying assets (Borrowers) make periodic monthly payments over the life of the loan that includes scheduled and unscheduled principal and interest. If payment is less than the interest then the outstanding principal will increase. The outstanding principal is revolving, not amortizing.

ABS is security that is backed by other assets. When these securities are collateralized by mortgages, they are called MBS.

A MBS is an ABS whose assets are mortgage loans. When these securities are collateralized by mortgages, they are called mortgage-backed securities (MBS), including commercial mortgage-backed securities (CMBS) and residential mortgage-backed securities (RMBS). In 1938, a governmental agency named the National Mortgage Association of Washington was formed and soon was renamed Federal National Mortgage Association (FNMA or Fannie Mae). It was chartered by the U.S. government as a corporation which buys Federal Housing Administration (FHA) and Veterans Administration (VA) mortgages on the secondary market, pools them, and sells them as MBS to investors on the open market.

SPV (SIV) issue and sell the MBS to investors. This allows for the issuing institution to be legally separated from the SPV. Mortgages are by far the most important underlying asset of global securitization, with residential mortgages being the most important single asset class. A bank provides mortgage loans to various homeowners A, B, etc., and puts these mortgages together in a pool of many mortgages. Subsequently, this bank that has originated these loans sells the pool of mortgages to a SPV, in return for cash. In this true sale securitization, the mortgage loans disappear from the balance sheet of the bank. In order to finance its purchase of the mortgage pool, the SPV issues residential MBS and sells these securities to various investors. The residential MBS sold are tranched in specific classes according to their credit risk, such as rated by the CRA. Thus, a tranche can be defined as a specific portion of a securitized portfolio of assets, based on a group of assets with similar credit risk characteristics. On the basis of a pool of mortgages of U.S.100 million, RMBS are created which consist of U.S.60 million of investment grade securities, subdivided in tranches rated super-senior AAA, senior AA and mezzanine BBB, and of U.S.40 million of below investment grade securities, with tranches rated subordinated B and unrated (the so-called equity tranche). According to their specific risk preferences, various types of investors buy specific tranches.

MBSs are a perfect example of securitization. By combining mortgages into one large pool, the issuer can divide the large pool into smaller pieces based on each individual mortgage's inherent risk of default and then sell those smaller pieces to investors. MBS had enabled financial institutions and investors around the world to invest in the U.S. housing market.

A short—term investment instrument with a maturity that is typically between 90 and 180 days. The security itself is typically issued by a bank or other financial institution. The notes are backed by physical assets such as trade receivables, and are generally used for short—term financing needs. ABCP is a form of commercial paper that is collateralized by other financial assets. They are designed to be used for short—term financing needs. SPV [SIV) issue and sell the ABCP to investors. This allows for the issuing institution to be legally separated from the SPV.

A company looking to enhance liquidity may sell receivables to a bank or other SPV (SIV), which, in turn, will issue them to its investors as commercial paper. The financial assets that serve as collateral for ABCP are ordinarily a mix of many different assets, which are jointly judged to have a low risk of bankruptcy by a ratings agency. However, in 2008 many of these assets performed more poorly than expected, making buyers much less willing to purchase ABCR As markets became unwilling to purchase ABCP, this caused trouble for financial institutions that had relied on sales of ABCP to obtain funds for use in longer—term investments. The liquidity and solvency concerns regarding key financial institutions drove central banks to take action to provide funds to banks to encourage lending to worthy borrowers and to restore faith in the ABCP markets, which are integral to funding business operations. Certain investors, or collateral providers which can be banks or other entities, want to obtain financing by selling certain assets to an ABCP SIV.

Collateralized debt obligations are backed by subprime— mortgage bonds, commercial—mortgage loans and other assets. CDO do not specialize in one type of debt but are often non-mortgage loans or bonds. CDO are unique in that they represent different types of debt and credit risk. In the case of CDO, these different types of debt are often referred to as tranches. Each tranche has a different maturity and risk associated with it. The higher the risk, the more the CD0 pays. SPV (SIV) issue and sell the CD0 to investors. This allows for the issuing institution to be legally separated from the SPV.

The SPV finances its purchase of the pool by issuing a CDC in the form of tranched notes, which are bought by various investors. According to their risk preference, these investors buy either lower or higher—rated tranches, with corresponding higher or lower yields.

These structured CDOs are based on the securitization of another securitization, for example a CDO based on mortgage-backed securities (i.e. CDO of MBS, which is called a collateralized mortgage obligation or CMO). Another example of a structured CDO is a CDO based on Other CDO, which is called a CDO2.

CDO are constructed from a portfolio of fixed—income assets. CDO are divided by the issuer into different tranches: senior tranches (rated AAA], mezzanine tranches (AA to BB], and equity tranches (unrated). Losses are applied in reverse order of seniority and so junior tranches offer higher coupons [interest rates) to compensate for the added default risk. Since 1987, CD0 have become an important funding vehicle for fixed- income assets.

This section explains and details the securitizations, which have played the most prominent roles in the subprime mortgage crisis of 2008. There are two types of credit derivatives: CD3 and synthetic CDO.

A credit default swap, or CDS, is essentially an insurance policy on a bond acquired by investors to guard against default. AIG wrote tens of billions of dollars worth of these contracts. Credit default swaps are often used to manage the risk of debt default. Under such a credit default swaps, the credit protection seller receives periodic cash payments, called premiums, in exchange for agreeing to assume the risk of loss on a specific asset in the event that asset experiences a default or other credit event. The CDS "buyer" is buying protection and the CDS "seller" is selling protection against a default or other credit event with respect to the underlying debt obligations (underlying asset). The buyer pays the seller a premium for this protection and the seller only pays the buyer if there is a default or other credit event that triggers the CDS contract. The premium the cost of protection for the buyer increases as the risk associated with the underlying obligation increases. In other words, as the credit worthiness of the underlying entity goes down, the cost of protection goes up. CDS are insurance contracts typically used to protect bondholders or MBS investors from the risk of default. This created uncertainty across the system, as investors wondered which companies would be forced to pay to cover defaults.

CDS can be bought by any investors including the underwriter [e.g., investment bank), the asset manager, the trustee and collateral administrator; it is not necessary for the buyer (i.e., Bear Stearns Wachovia, Citigroup. Deutsche Bank, and Merrill Lynch) to own the underlying credit instrument. Like all swaps and other financial derivatives, CDS may either be used to hedge risks (specifically, to insure creditors against default) or to profit from speculation. The volume of CDS outstanding increased 100-fold from 1998 to 2008, with estimates of the debt covered by CDS contracts, as of November 2008, ranging from U.S. $33 to $47 trillion. CDS are lightly regulated. As of 2008, there was no central clearinghouse to fulfil CDS in the event a party to a CDS proved unable to perform his obligations under the CDS contract. Required disclosure of CDS-related obligations has been criticized as inadequate. Insurance companies such as AIG faced ratings downgrades because widespread mortgage defaults increased their potential exposure to CD3 losses. These firms had to obtain additional funds (capital) to offset this exposure. AIG has having CDS insuring $440 billion of MBS resulted in its seeking and obtaining a Federal government bailout. AIG destroys itself by selling mispriced CDS. The blunders of the AIG, the world's largest insurance company, offer the first—ever instance of an institution that is "too interconnected to fail" acting to devastate itself, its shareholders, U.S. taxpayers, and the greater financial system simply by the misuse of CDS. As a result, one of the most successful companies in business history, with over $1 trillion in assets, has been almost entirely nationalized.

Like all other pure gambles, what one party loses under a CDS, the other party gains; CDS merely reallocate existing wealth. Hence the question is which side of the CDS will have to pay and will it be able to do so. When investment bank Lehman went bankrupt in September 2008, it created a great deal of uncertainty regarding which financial institutions would be required to fulfil the CDS contracts on its $600 billion in outstanding debts. Significant losses at investment bank Merrill Lynch were also attributed in part to CDS and especially the drop in value of its unhedged mortgage portfolio in the form of Collateralized Debt Obligations after AIG ceased offering CDS on Merrill's CDO.

Securitizations can be conducted basically in two ways. First, in a so-called true sale securitization, the underlying assets are indeed actually sold by the originators (i.e., bank) to the SPV and thus removed from the balance sheet of the originator. Second, in a so-called synthetic securitization, the underlying assets remain on the balance sheet of the originator, and only the credit risk of the underlying assets is transferred to the SPV by buying credit derivatives such as credit default swaps over this assets.

Similar to securitizations, in addition to "cash flow" CDO, there also exist "synthetic" CDO, where the SPE/SPV does not buy physically the portfolio of underlying debt instruments, but sells credit default swaps over the same debt instruments underlying the "cash flow" CDO described above. Thus, the SPE/SPV receives periodic cash payments and bears legal liability without owning the underlying debt, and issues a synthetic CDO to investors.

The originator buys protection through a CDS contract from the SPE/SPV, which is the seller of protection and gets a CDS premium to bear legal liability of the underlying debt. The SPE/SPV transfers the credit exposure by issuing CDO tranches and selling it to investors (through the same process as in the "cash" CDO]. If a default event occurs to the underlying debt, the SPE/SPV pays the CDS protection to the originator. "Synthetic" CDO played a rather active role in the propagation of the financial crisis. In the context of actual and feared further downgrades of various financial guarantors and of CD0 by the CRA, a rapid unwinding of "synthetic" CDO positions by in particular hedge funds resulted in a further widening of credit spreads, as demand for these products collapsed. This process spilled over to other securitization products such as residential and commercial mortgage—backed securities [RMBS and CMBS] and other asset-backed securities.

Many U.S. mortgages issued in recent years are subprime, meaning that little or no down payment was made, and that they were issued to households with low incomes and with troubled credit histories. Subprime mortgages are residential loans that do not conform to the criteria for prime mortgage and so have a lower expected probability of full repayment, because they are made to more risky mortgage borrowers. This assessment is made according to objective criteria such as the borrower's credit score record and loan-to—value ratios. Subprime mortgage borrowers have a less than perfect credit history and are required to pay interest rates higher than what would be available to a traditional agency borrower. Between 2001 and 2008, poor underwriting standards and excessive lending led to a very large number of default-prone home mortgages.

If a borrower is default in making timely mortgage payments to the loan lender, the lender can take possession of the residence and call a foreclosure. The Subprime Mortgage Crisis of 2008 arises because a borrower has the option of defaulting on the loan he owes. Typically, lenders (who were primarily thrifts) undertake the default risk on the mortgages they issued. Over the past 60 years, a variety of financial innovations have gradually made it possible for lenders to sell the right to receive the payments on the mortgages they issue, through a process called securitization. The resulting securities are called MBS. Investors in MBS can insure against default risk by buying CDS.

Credit-default swaps ["CDS") are a valuable financial tool that has created system—wide benefits. At the same time, however, these derivative contracts have also created the potential for relatively few market participants to destabilize the entire economic system. CDS helped support the growth of the sub—prime mortgaged—backed securities asset bubble that has been blamed for igniting the current financial crisis. Although CDS are a valuable tool that has traditionally helped businesses efficiently allocate risk, they do create systemic danger in several ways, some of which have become manifest in the past year. As a result, CDS have intensified the scope of the financial crisis.

As mortgage defaults rose, the likelihood that the sellers of CDS would have to pay their buyers increased. This created uncertainty across the system, as investors wondered if CDS sellers would fulfill their promises. The scope of this crisis were much larger than had been anticipated, due to information indicating further deteriorating conditions in U.S. subprime mortgage markets. Central banks around the world cut interest rates and governments implement economic stimulus packages. These actions were designed to stimulate economic growth and inspire confidence in the financial markets. But uncertainty in securitization markets remained at elevated levels. There is broad consensus that securitization played an important role in the propagation of the subprime mortgage crisis. The subprime mortgage crisis revealed a number of weaknesses of securitization. Banks underestimated and invested too much in securitization instruments.

The author wants to conclude this article with a short discussion of the role of the CRA in securitization and the financial crisis. The financial crisis of 2008 has revealed substantial shortcomings of the global financial system.

Those shortcomings are all about securitization. Those shortcomings have in particular been in the process of the securitization; CRA are of enormous importance, as they rate the bank that originates the securitization, the SPV that creates the securitization and the specific tranches of the securitization. Most investors trust those ratings; however most of those ratings are trustless. This article is to present the fundamentals of securitization and their role in the financial crisis. As aforementioned, financial crisis comes from securitizations. Thus, securitizations played a crucial role in the development and propagation of the financial crisis.

Essentially, the financial crisis highlighted strong doubts on the ratings methodologies for securitization products. These doubts further increased by substantial ratings‘ downgrades both in number and severity in the course of 2008. The crisis revealed intrinsic problems with the valuation of securitization products and various incentive problems involving the CRA.

In hopes of minimizing further systemic collapse, this Paper recommends that securitization (e.g., CDS) become regulated in a way that balances the efficiency of a free market with the goal of economic stability.