A Study on The Relevance of Technical Analysis In Detecting Trading Signals In Indian Equity Markets

Pavankumar Chandrappa * Triveni P.

* Subject Matter Expert- Financial Services, iNurture Education Solution Pvt Ltd, Bengaluru, Karnataka, India.

** Assistant Professor and Head of Research Division, M.S. Ramaiah Institute of Management, Bengaluru, Karnataka, India.

Abstract

Often, investors, especially retail investors are confused about the relevance of technical analysis in equity analysis. The usefulness of the concept has been debated, deliberated and censured by several scholars. The fundamental analysts have shunned the theory stating that technical analysis is similar to astrology. Some of the studies conducted by the scholars from universities like Stanford, Oxford, and Massachusetts Institute of Technology during 1960's have shown that technical analysis tools are not effective in generating consistent trading signals. Despite all these eruptions, the concept of technical analysis is becoming popular amongst traders and investors. The proposed study attempts to contribute to the ongoing discussions about the relevance of technical analysis in detecting trading signals in stock markets. The study would have an enormous practical impact on investors and brokers and the way they approach the market. The study also tests the scientific orientation behind the technical indicators and some of the strong deliberations happening around the concept.

Keywords :

- Technical Analysis,

- Technical Indicators,

- Trading,

- Wall Street,

- Demand,

- Supply,

- Market Efficiency

- Prediction,

- Price Behaviour

- Stock,

- Prices,

- Markets,

- Fundamentals,

- Equity

Introduction

What determines the price of a stock? How to determine the price of a stock? Probably, there would be different claims on these questions from different individuals. The answer completely depends on whom the question is asked. A fundamental analyst would probably claim that the changes in the price are the function of financial condition and profitability of the company (Turner, 2007). He believes that there are cause and effect relationship which exists between fundamentals and the stock price. That means, if the fundamental news about the stock is positive, the price will shoot up and vice versa. If the same question is routed to a technical analyst, perhaps he would claim that the change in the price of a stock is the function of historical prices. The technical analyst uses a variety of technical tools to draw the conclusion. They may claim that the historical price and volume of trade determines the price of a stock. These two conclusions are based on their philosophy or ideology rather scientifically tested evidence. It is not about who is right, but what is right, that is of the most important in this context. Yet, it is a debatable question since decades.

The concept of technical analysis of stocks has seized the attention of both academicians and practitioners for years. The key principle of the technical analysis is that the stock market is made of a human being and the behavior of a human being is dynamic. The dynamic behavior of a human being will have an impact on the stock prices. Markets are influenced by emotions, greed, fear and other psychological aspects of a human being (Shiller, 2003). The theory of Technical Analysis is based on three important assumptions which are as follows (Murphy, 1999).

- The market discounts everything.

- Price moves in trends.

- History tends to repeat itself.

The Market Discounts Everything

Dow Theory advocates that, at any given point in time, a stock's price reflects all available information including fundamental information. The information contains a whole lot from emotions of investors to interest, inflation data along with pending earnings announcements to be made by companies after the close. Technical analyst advocates that the company's fundamentals are priced into the stock, removing the need to actually consider these factors individually in the form of fundamental analysis. According to this postulation, the information excluded only of uncontrollable in nature. For example, earthquake, government policies, global economic crisis, etc.

Price Moves in Trends

The technical analyst believes that the prices of securities move in trends. That means, as soon as the trend is established, the future price movement is most likely to be in the same direction as the trend to be against it. Most of the technical trading strategies are built based on the premise. Dow believed that the laws of action and reaction apply to the markets just as they do in the physical universe

He wrote, "Records of trading show that in many cases when a stock reaches the top it will have a moderate decline and then go back again to near the highest figures. If after such a move, the price again recedes, it is liable to decline some distance."

The major rationale behind the graphical representation of price action is to identify trends at an early stage as they are being formed. These trend directions are then used to trade the security. A trend is expected to continue till it reverses. So, continuous study of trends is necessary to spot the reversals at an early stage. The trends are not only up or down, they can be sideways also.

History Tends to Repeat Itself

The third most important assumption of the Dow Theory is that the history tends to repeat itself particularly in terms of price movements. The recurring nature of price movements is attributed to market psychology. Market participants have a propensity to provide a consistent reaction to similar market stimuli over a period of time. Technical analysis uses chart patterns to analyse the market movements. For example, let us assume, there was a lot of selling that had happened at the price  50 previously and because of the selling, the prices had fallen further. It would be again the case as and when the price approaches 50 levels even today. As the behaviour of the investors often repeats itself, Technical Analysts also believe that recognisable price patterns will ultimately develop on a chart.

50 previously and because of the selling, the prices had fallen further. It would be again the case as and when the price approaches 50 levels even today. As the behaviour of the investors often repeats itself, Technical Analysts also believe that recognisable price patterns will ultimately develop on a chart.

Charles Dow developed a hypothesis that the stock market does not move on a random basis, but they are influenced by three unique cyclical trends that guide its direction. A few of the important aspects of this study, including the market efficiency, technical trading tools, and their impact on stock prices are much debated in American stock markets. The countries with advanced stock markets like the United States will have an edge in terms of market efficiency compared to the developing economies. The Wall Street has run a series of experiments to detect trading signals using technical analysis and found it useful.

It is essential to note that, the technical analysts do not deny the role of the fundamental factors in the stock price analysis. Instead, they argue that, all the fundamental factors, including the publicly available information about the stock is already discounted in the prices. Hence, there is no need to evaluate the fundamentals separately. This is one of the most important reasons for the attractiveness of technical analysis.

The progressive financial markets like the United States and the United Kingdom has been found to be most efficient due to the extensive use of cutting-edge technology in trading activities. Several equity analysts from these countries have shunned the concept of Technical analysis. Yet, the emerging markets like India have found to be profitable. Several studies have been undertaken by technicians and revealed that technical analysis generates substantial trading signals in the financial markets (Sullivan, R., A. Timmermann, and H. White, 1999).

1. Review of Literature

1.1 Early 1990s

Empirical evidence from many recent studies has shown that returns are predictable from the current price, past prices and other variables like volume, etc. These studies pose a series of challenges to the efficient market hypothesis (Fama, 1965). Michael D. Goldberg and Schuhneister (1988) argue that the technical rules examined are considerably more profitable with hourly data than they are with daily data. Though a large number of investigations on the predictability of the equity returns have so far been carried out, the numbers of such investigations that have scrutinized Technical Analysis as a means of predicting stock prices or equity returns are relatively petite. Nevertheless, the fact may not be surprising due to the concept of Technical Analysis was seriously criticized on the grounds of Efficient Market Hypothesis (Fama,1965). Despite its theoretical beauty, Eugene Fama claimed that technical trading rules do not work. However, literature has been divided into two segments. There are several researchers and traders who have found the evidence on the predictability of the technical tools.

1.2 Recent Empirical Works

This segment of the paper throws light on the recent empirical works undertaken in the field of Technical Analysis. This is intended to stress on the recent developments on the purification, simplification and modifications, technical testing procedures and also to give a perspective on the shifts taken place in the area of Technical Analysis of Stock markets.

It is also observed that technical analysis can generate higher returns than a traditional “buy –hold” strategy (Papadamou and Tsopoglou, (2001). Burton G. Malkiel (2003) investigated that in every case, the market did correct itself. The market eventually corrects any irrationality-albeit in its own slow, inexorable fashion. Anomalies can crop up, markets can get irrationally optimistic, and often they attract unwary investors. But ultimately, the intrinsic value is recognised by the market, and this is the central lesson investors must note (Malkiel, B. G., 2003). Clare Dixon (2005) noted a divergence in thought between economists and technicians in that excess returns from using technical analysis techniques are incompatible with the efficient market hypothesis and also observed that the markets may not necessarily be perfectly efficient. The paradox of efficient markets has shown us that in order to collect and analyze costly market data to the extent that investors do, they must receive some reward in the form of increased profits or it would not be profitable to perform the analysis at all (Dixon, C., 2005). Chang et al. (2006) and Metghalchi et al. (2009) also supports the view expressed by Chang and Metghalchi. Park and Irwin (2004) examined the profitability of trading rules in the US futures market and reported that the technical trading rules are not profitable in the US futures market. In the same year, Chong et al. (2010) applied four well-liked technical indicators on the stock markets of the BRIC countries and concluded that the technical indicators are valuable even after the consideration of the transaction costs. Metghalchi and Garza-Gomez (2011) applied technical tools on Abu Dhabi Stock Index and concluded that the technical trading rules are insignificant compared to buy-hold strategy. The technical analysis gives an investor a better understanding of the stocks and also gives a right direction to go on further to buy or sell the stocks (R. Chitra, 2011). The simple moving average was able to generate the sell signal, but only after four days and after the start of the crash. Thus, to the extent that time lap parameter is considered, Simple Moving average has been constantly giving a good performance, for prediction of crashes in stock markets. P. Nageswari and Selvam, M. (2011) investigated the existence of seasonality effect on stock returns for BSE Sensex index. The study found that there was a maximum return earned on Wednesday and negative returns recorded on Monday during the study period. Metghalachi et al., (2012) further extended their research and used moving averages for 16 European countries and found that technical trading rules are able to detect trading signals in smaller exchanges.

Often, technical tools give hilarious trading signals if used in isolation. For example, when the moving averages generating sell signals for a stock, the Relative Strength Index for the same stock may generate the buy signal. This is due to the embedded nature of test ability of each technical tool. To overcome this sticky situation, Loh (2007) has tested the validity of technical trading rules in the combination of moving averages, stochastic oscillators, and trend indicators. He had identified that the combined trading rule considerably improve the trading returns in five Asian markets. Bajgrowicz and Scaillet (2008) re-examined the noticeable success of technical trading rules of daily prices of Dow Jones Industrial Average (DJIA). They concluded that even if some technical tools are effective in detecting trading signals, it is not possible to outperform market due to transaction costs involved in each trading activity. That means the trading results was achieved using technical tools offset against the transaction cost. Hence, there is no point in applying technical tools in equity analysis. The only way to make high returns is by investing in risky investment options. Toni Turner explains the situation with an example where greed takes hold of the investors and traders. He says that “Say you buy a stock at the perfect entry point. Within minutes, the price rises even higher than you expected. A little voice whispers in your ear, this baby's gonna fly. Why don't you take all the money in your trading account and buy as many shares as you can? You'll make a killing!” (Turner, 2007). Panicky, on the other hand, might lead traders to sell shares ahead of time. Irrational behavior in the market thus leads to profitable situations if detected. Price patterns are designed to determine this ludicrousness when greed and fear take the grip of a stock. Toni Turner (2007) clarifies that any triumphant trader needs to gain knowledge of how to control these emotions and rather rely on detecting when they occur in the market. In our case, a potential artificial trader is luckily endowed with a sense of bit-calculating rationality.

2. Objectives of the Study

- To contribute to the ongoing discussions about the relevance of technical analysis in detecting trading signals in equity markets.

- To test the scientific orientation behind some of the strong deliberations happening around the concept.

- To analyze the empirical results to identify the realism of technical analysis.

- To examine the importance of demand and supply in technical analysis of stocks.

3. Scope of the Study

The study is circumscribed to analyse the results of empirical studies in order to understand the perspectives of various research scholars in the area of technical analysis towards the relevance of technical indicators in equity analysis. The study investigates a couple of important economic aspects (i.e. demand and supply) and their relevance in stock price movement.

4. Research Methodology

The proposed study is focused on qualitative aspects of the research problem. The study gathers the data that describes the market movements using the concept of technical analysis. The study uses an in-depth narrative description of research articles, dissertations as a tool to organise the data into patterns in technical analysis. These patterns aid an investor in comprehending the behaviour of stock prices in financial markets. Meanwhile, the human mind cannot extract the full import of a large mass of raw data and numbers, analysis has been carried out in simple language. A visual aid is used to describe an important element in technical analysis. The citations provided within the research are published by prestigious and highly quality oriented journals. Hence, it can be deducted that the propositions in the research are dependable.

4.1 Sampling Technique

The simple random technique has been used to pick up research articles in the area of technical analysis.

5. Discussions

Over the past few years, there has been a rise in the popularity of this approach. Several books have been published from the successful technical traders. The books have been welcomed by the academic world. The successful technical traders believe that the overall investor's expectations, optimism, pessimism drive the market and prices. These psychological aspects can be traced using technical indicators and tools. Therefore, it is rightly called as the “study of mass investor's psychology”. Most investors would claim that financial parameters have a bearing on the price. Technical analysts would rely on the historical prices to determine trends. The skeptics have, however, questioned the validity of some aspects of technical analysis. They dispute its validity on the ground that it is an art. This is partly due to the perception in the minds of investors that technical analysis is only as good as the person interpreting it. This criticism is more a reflection of the manner in which it is applied rather than that of technical analysis by itself.

The concept of technical analysis has also been criticized on the grounds of scientific validity. The studies examining the effectiveness of Technical Analysis can be traced back to the 1960s. Most of the research work during that time was shunned under the shades of Efficient Market Hypothesis (EMH). Nevertheless, the research undertaken after the 1970s has given a significant push for the argument that technical tools are able to detect trading signals using time series data. Equivalent to that the growing number of profitable trading signals generated by the technical tools has posed series of questions on the EMH theory. The Wall Street has run a series of experiments to test the validity of technical analysis and found it useful and reliable. The profitability of technical tools was visible during the 1980s. Nonetheless, the serious doubts on the validity of the concept ‘technical analysis’ was arisen during mid of 1990s to present. This was due to the advanced financial markets and improved market efficiency, the self-destructive nature of technical tools, data snooping and many other factors.

Further, the theory disputes that a human cannot work like a robot. He/she changes behavior on the basis of what he/she sees, hears and experiences. Certain actions of human beings are programmed to create same responses from individuals. Richard Demille Wyckoff, one of the pioneers in the field of technical analysis contends that technical analysis is highly reliable. He bases his argument on the proposition that technical analysis is based on price movement and therefore a reflection of demand and supply in the market. His contention is that stock prices are a more realistic indicator of investor sentiment and the state of an economy as compared to fundamentals. He further averse that fundamentals are built into the price and therefore price movements are a better indicator of future prices.

Charles Dow, William Delbert Gann, Ralph Nelson Elliot, Merrill Lynch, and Richard Wyckoff - considered five 'titans' of technical analysis – have provided theoretical insights and practical approaches on the various aspects of technical analysis. Many of Wyckoff's postulations have become de facto standards in technical analysis. The notion of accumulation and distribution is a seminal contribution of Wyckoff to the theory of technical analysis. Steve Nison, a practitioner of technical analysis, exemplifies the importance of technical tools by relating it to their effectiveness in identifying entry and exit points.

Despite its academic richness and frequently proven applicability in equity analysis, the concept of technical analysis has been contentious for decades. There are thousands of technical tools available in financial markets. Not all the tools are effective in trading activities. Some of the tools are irrelevant in today's vibrant financial markets. This does not invalidate the reliability of technical analysis as a forecasting tool. There is no gainsaying the fact that demand and supply indicate the mood of the market. Some scholars argue that a mere analysis of demand and supply of stocks may be insufficient to detect trading signals in the dynamic financial markets. The demand and supply approach is also subject to the vagaries of market manipulation.

Technical indicators reflect human behavior and any study of technical analysis has to study its concomitant constituent, i.e. the investor. A few of the important aspects of the proposed study, including the market efficiency, technical indicators and their impact on stock prices are much debated in American stock markets. Further, the Wall Street has run a series of experiments to detect trading signals using technical analysis and found it useful.

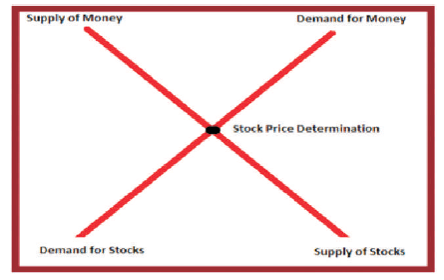

Nonetheless, Richard Demille Wyckoff - one of the five 'titans' of technical analysis along with Charles Dow, Gann, Elliott, and Merill have provided theoretical and practical approaches to the stock market analysis using the concept ‘technical analysis’. Richard Demille Wyckoff argues that supply and demand are the two important elements in the stock price determination. The supply and demand are the two fundamental factors in economic theory and also can be considered as the backbone of fundamental forecasting (Murphy, 1999), though it is highly debated amongst the traders. They argue that a mere analysis of demand and supply of stocks may be insufficient to detect trading signals in the dynamic financial markets. The study of stock markets is no more restricted to the traditional theories based on demand and supply. Because, the financial markets are often manipulated by pseudo investors. Even if there are no significant changes in the level of supply and demand for the stock, the prices have been manipulated by a certain group of investors. Further, as shown in Figure 1, there are two other critical components such as demand for money and supply of money which also plays a crucial role in the stock market analysis. The point where demand (stocks), supply of stocks, supply of money and demand for money intersects is the point at which the stock price is determined unfortunately, these two unique elements are hardly debated in the academic world.

Figure 1. Demand for Money and Supply of Money

It is important to note that; technical analyst does not counter the importance of fundamental factors related to the market. But, they believe that the publicly available information is already discounted in the price data. Hence, there is no need to separately analyse fundamental factors, including demand and supply in the stock market analysis.

Despite all these factors, markets are efficient with a certain amount of inertia. The market is made of a human being and the behavior of human beings is dynamic. A human cannot work like a robot. This dynamic behavior will have an impact on the prices in the market. Certain actions of human being are programmed to create the same response from an individual. The psychological factors impact the stock prices; hence, it is rightly defined as the “study of mass investor's psychology”. The behavior of an investor changes based on what they see, hear and experience. The successful technical traders argue that the overall investor's expectations, optimism, pessimism drive the market and prices. This is the most important reasons for the popularity of the concept ‘technical analysis’.

The first censure of the Dow Theory is that it is really not a theory, as neither Dow nor Hamilton published any academic papers setting out the theory. The theory was never tested by either of them. The Dow Theory was made known to the world through a series of editorials in the Wall Street Journal. Later on, Robert Rhea formulated the theory by reading and analysing the large volume of editorials written by Dow and Hamilton.

The second criticism is that the trend change indicators are too late. The trend does not change from bearish to bullish until the previous high has been broken. Many market players feel this is too late to enter the market. What Dow and Hamilton advocated was entering the market at the participating phase of the trend. Also, Dow Theory says that “the averages must confirm each other”. So, if one waits for the other averages to confirm the move, the entry into the market would be even later. The response to the above criticism is that it was never intended by Dow to anticipate trends. What he wanted to do was to capture the second phases, which is the participating phase of a trend.

Thirdly, the Dow Theory is criticised as being outdated and no longer an accurate reflection of the economy. This is mainly because it still uses the Dow Jones Industrial Average (DJIA) and Dow Jones Transportation Average (DJTA). Still, it is essential to note that these two averages are one of the most economically sensitive indices and reinforces the view that the stock of economic growth. To keep the DJIA relevant in today's world, new stocks are added to replace old stock in the calculation of the average.

6. Suggestion

Based on the experiences, the practitioners have given some of the recommendations for investors. The following are some of the common guiding principles:

- Believe in the concept of “Trend is your friend”

- Stay away from the correcting markets

- Be selective to identify the right market and script

- Trade only if the stock is highly liquid

Conclusion

For all the criticisms, the technical analysts have given befitting responses with proven evidence. They have garishly depicted the expediency of technical analysis with real-time proofs. The technical traders strongly believe that in stock market analysis “what” is more important than “why”. The reputation of the concept has been grown substantially in the past 15 years. This is evident by the fact that most of the TV Channels, Newspapers are now posting trading recommendations based on technical analysis. On the top of it, the number publications and research in the field of technical analysis is rising endlessly. Despite its frequently proven applicability in equity analysis, the concept of technical analysis has been contentious for decades. Three important questions which are still buzzing in our ears;

- Are technical indicators relevant in detecting trading signals?

- Does inefficiency exist in advanced equity markets?

- Is technical analysis a self-defeating prophecy?

The vacillation around these questions has put investors in a quandary – Do investors still rely on technical analysis? There is a gap to conduct research and subtle nuance residing in the field of technical analysis of stocks.

References

[1]. Bajgrowicz, P., & Scaillet, O. (2008). Technical Trading Revisited: Persistence Texts, Transaction Costs, and False Discoveries. HEC.

[2]. Chang, Y. H., Metghalchi, M., & Chan, C. C. (2006). Technical trading strategies and cross-national information linkage: The case of Taiwan stock market. Applied Financial Economics, 16(10), 731-743.

[3]. Chitra, R. (2011). Technical Analysis on Selected Stocks of Energy Sector. International Journal of Management & Business Studies, 1(1), 42-46.

[4]. Chong, T. T. L., Cheng, S. H. S., & Wong, E. N. Y. (2010). A comparison of stock market efficiency of the BRIC countries. Technology and Investment, 1(04), 235.

[5]. Dixon, C. (2005). Can Technical Analysis Disprove the Efficient Market Hypothesis? A Foreign Exchange Example (Bachelor's Thesis).

[6]. Fama, E. F. (1965). The behavior of stock-market prices. The Journal of Business, 38(1), 34-105.

[7]. Goldberg, M. D., & Schuhneister, S. (1988). Technical Analysis and Stock Market Efficiency from http://typo3.wsr.ac.at/schu/fileadmin/homepage_schul meister/files/TechnicalAnalysisAndStockMarketEfficiency. PDF

[8]. Loh, E. Y. (2007). An alternative test for weak form efficiency based on technical analysis. Applied Financial Economics,17(12), 1003-1012.

[9]. Malkiel, B. G. (2003). The efficient market hypothesis and its critics. The Journal of Economic Perspectives, 17(1), 59-82.

[10]. Metghalchi, M., Du, J., & Ning, Y. (2009). Validation of moving average trading rules: Evidence from Hong Kong, Singapore, South Korea, Taiwan. Multinational Business Review, 17(3), 101-122.

[11]. Metghalchi, M., & Garza-Gomez, X. (2011). Trading rules for the Abu Dhabi stock index. Review of Middle East Economics and Finance, 7(1), 52-66.

[12]. Metghalchi, M., Marcucci, J., & Chang, Y. H. (2012). Are moving average trading rules profitable? Evidence from the European stock markets. Applied Economics, 44(12), 1539-1559.

[13]. Murphy, J. J. (1999). Technical analysis of the financial markets: A comprehensive guide to trading methods and applications. Penguin.

[14]. Nageswari, P., & Selvam, M. (2011). An empirical study on seasonal analysis in the Indian Stock Market. International Journal of Management & Business Studies, 1(4), 90-95.

[15]. Papadamou, S., & Tsopoglou, S. (2001). Investigating the profitability of technical analysis systems on foreign exchange markets. Managerial Finance, 27(8), 63-78.

[16]. Park, C. H., & Irwin, S. H. (2004). The profitability of technical analysis: A review. AgMAS Project Research Report No. 2004-04.

[17]. Shiller, R. J. (2003). From efficient markets theory to behavioral finance. The Journal of Economic Perspectives, 17(1), 83-104.

[18]. Sullivan, R., Timmermann, A., & White, H. (1999). Data-snooping, technical trading rule performance, and the bootstrap. The Journal of Finance, 54(5), 1647-1691.

[19]. Turner, T. (2007). A Beginner's Guide To Day Trading Online, 2nd Edition. Simon and Schuster.