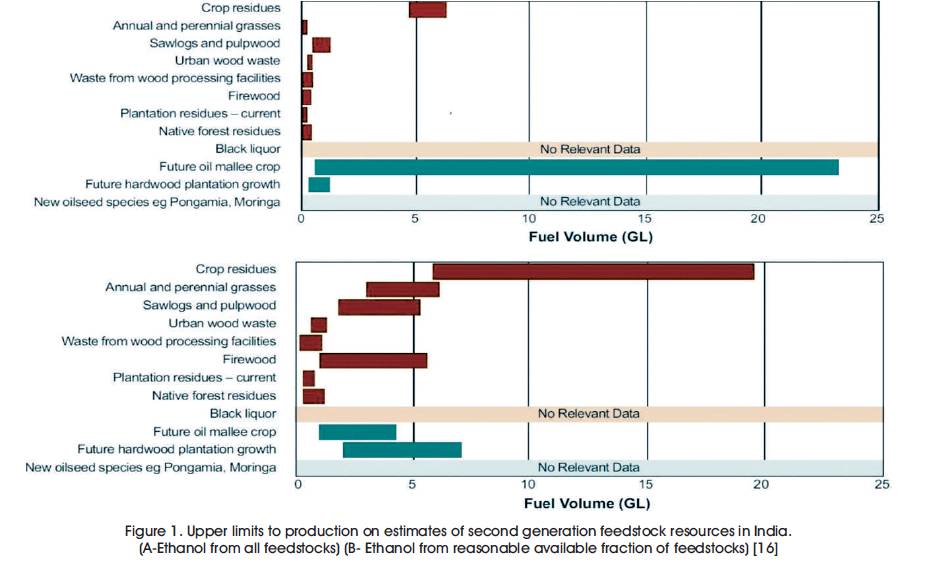

Figure 1. Upper limits to production on estimates of second generation feedstock resources in India. (A-Ethanol from all feedstocks) (B- Ethanol from reasonable available fraction of feedstocks) [16]

Consequent to rising oil prices and growing fears of climate change, biofuels are receiving increasing consideration worldwide as alternative to fossil fuels. Biofuels are being considered as sustainable alternatives to fossil fuels, because of their potential to promote energy security and reduce greenhouse gas emissions. At the same time, biofuels also provide opportunities for job creation and diversification of rural economy. Hitherto the large-scale production of biofuels requires shift from our current dependence on fossil fuels and brings with it a suite of potential problems. Second generation biofuels derived from ligno-cellulosic agricultural residue are increasingly attractive to the biofuel industry because they are expected to be more efficient than first generation crops and they will not compete directly with food production.

The aim of this review is to provide an overview of the second generation biofuels in an Indian context and to describe the barriers to wider adoption of the biofuels. This review also aims to appraise the development of second generation biofuels industry in India summarizing the approximate costs for commercial scale plants from the literature along with major commercial and research programs in second generation fuels production in the country. This paper lists Indian research and development gaps that, once overcome, should assist in taking the industry forward. An objective of the review is to stimulate policy makers and industry to examine more closely the opportunities in second generation biofuels that are unique to India.

International Energy Agency (IEA) estimates that a 50% reduction in Green House Gas (GHG) emissions by 2050 will require an increase in bioenergy production by a factor of four, to 150 EJ/year (1 EJ = 1018 Joules), providing more than 20% of the world is primary energy [1]. With both agronomic and societal concerns about increase in the use of grains and oilseeds for biofuels, bioenergy will likely be coming from ligno-cellulosic feedstock, dedicated energy crops, agricultural residues, forests and organic wastes. The biofuels obtained from those sources have been denoted as second generation biofuels. Both developed as well as developing countries are placing greater emphasis on Second Generation biofuels as an alternative to fossil fuels. By 2020, European Union (EU) legislation necessitates that, 20% of energy must be produced from renewable sources, with 10% of transport energy (final use) derived from a renewable source (EU, Directive 2009/28/EU). The USA has similar legislation in place that calls for 136 Giga Liters (GL) of renewable liquid fuel to be used by 2022 (USA, Public Law 2007/110- 140/USA). Other countries targeting biofuels include, China, Canada and Brazil, and the level of interest is such that the International Energy Agency (IEA) projects a five-fold increase in global biofuels production by 2030 [2, 3].

According to IEA, global bioenergy resources are more than sufficient to meet projected biofuels and biomass supply without competing with food production [3]. Policy measures should be very selective in promoting only those biofuels technologies that substantially contribute to emissions reduction, avoid adverse land and water uses, and have positive social impacts.

India is one of those countries that are considered rich and abundant in fossil fuel energy resources. It is important for India to regulate the use of conventional energy and attempt to replace these conventional energy resources with Renewable Energy (RE) resources. Recent studies [4-23] highlighted the current status, progress and prospective of renewable energy alternatives in India. India is the world's 8th-largest primary energy consumer. There are two major issues regarding transport of fuels faced by most of the countries in the world, including India.

Bioethanol from lingo-cellulose is a carbon-neutral, renewable source of energy. Additionally, second generation biofuel does not depend on a particular feedstock. It also stands to generate an additional source of income for the Indian farmers [4]. However, the production of ethanol from ligno-cellulosic biomass has various engineering and financial constraints. The cost of production of ethanol from ligno-cellulosic biomass depends on different variables, including the source and geographical location of feedstock, and the industrial route employed for the conversion of ligno-cellulosic biomass to ethanol.

The main fuels used for transport in India are Automotive Gasoline (petrol), Diesel Oil, Liquefied Petroleum Gas (LPG) and Aviation Turbine Fuel. Transport activity is expected to grow rapidly throughout the period, due to speedy population growth and increasing incomes. Road transport is projected to become more than double by 2050, shipping to triple, and rail and air transport to more than quadruple. Growth in light commercial vehicles and heavy trucks is expected to be faster than for private and passenger vehicles [26].

India currently imports 30% of its oil products which is projected to increase to 76% by 2030 [27]. Only about 0.5% of India's transport fuel is currently supplied from biomass. In India, the transport sector includes emissions from the direct combustion of fuels in transportation by road, rail, domestic aviation and domestic shipping.

Since 1990, emissions from the transport sector have increased by 47.5%, from 62.0 million ton (Mt) CO2 in the base year 1990 to 91.5 Mt CO2 in 2012 [28].

The transport sector is the largest end user of energy in India, consuming over one-third of the total energy, followed by the manufacturing and construction sector, and the residential, mining and commercial sectors. Fossil fuels accounted for about 96% of India's primary energy consumption and 90% of electricity generation in 2010–11. In 2010–11, India's consumption of refined liquid fuels was 52.1 GL. The transport sector is the largest final consumer of liquid fuels, accounting for around three-quarters of India's final fuel use [2]. The transport sector is the largest end user of energy in India. More than 38 % of India's final energy use is employed in moving people and goods across the country.

With the rapidly increasing worldwide demand for fuel and energy, it has been recognized that alternative, sustainable sources of transport fuels will be needed to ensure the security and longevity of supply. Ethanol has experienced unseen levels of attention due to its value as fuel alternative to gasoline [5]. Compared with gasoline fuel, ethanol fuel possesses greater combustion efficiency and minimal energy losses [6]. A mandate of 10% ethanol in all Indian petroleum sourced from first generation feed stocks would probably lead to a requirement to import grain in drought years. A potential solution to the high first generation feedstock price and limited supply is the development of second generation biofuels that utilizes non-edible plant materials, such as sugar cane bagasse, native grasses, native perennials, forestry waste, farm forestry, wheat straw, newsprint and cotton trash.

Transport sector accounts for 15.9% of India's GHG emissions. The Indian Government has set a 2020 goal of reducing GHG emissions by 5% from 2000 levels irrespective of actions by other countries, and by upto 15% or 25% under strict conditions relating to the extent of international action. As part of its plan to secure a clean energy future, the government has adopted a long-term target to reduce GHG emissions by 80% compared with 2000 levels by 2050 [9]. These goals will be reached through the measures implemented under the Government's Clean Energy Future Plan.

Bioethanol has been used in Germany and France as early as 1894 by the incipient industry of internal combustion engines. Brazil has utilized bioethanol as a fuel since 1925 [7]. The Brazilian Alcohol Program (Proalcohol) was established in 1975 for the purpose of reducing oil imports by producing ethanol from sugarcane [8]. The majority of post 1986 vehicles operating in India roads are suitable for use with ethanol in blends up to 10% ethanol. E10 is a blend of conventional petroleum with a 10% mass component of ethanol. Around 90% of ethanol produced by each year in India is being used in gasoline blends in the transport sector [5]. In India, first generation biofuels consist of ethanol produced from C-molasses and wheat starch byproducts and grain (mainly sorghum), and biodiesel predominantly produced from tallow (animal fats) and used cooking oil. As a result of the support from Central government in India, aimed pricing for biofuel is estimated to fall by as much as US$ 0.1176 per liter for ethanol and US$ 0.1796 per liter for biodiesel by 2015. Biofuels production for 2012 is estimated at 555 Million Liter (ML), comprised of about 440 ML of ethanol and 115 ML of biodiesel. The total operating biofuels production capacity in India is around 600 ML a year. Biofuel accounts for around 0.4% of the total transport fuel consumption. India's installed biofuel annual capacity is forecasted to rise to 1519 ML by 2015. Installed ethanol capacity was forecasted to rise to 910 ML by 2015 from 350 ML in 2010. The mandates, plus growing use of biofuels as alternative to crude oil-based fuel, would see biodiesel capacity rise to 609 ML by 2015 from 286 ML in 2010.

In general terms, first generation biofuels refer to those mainly based on sugar, grains, or seeds, and generally requiring relatively simple processing to produce the fuel. In contrast, second generation biofuels would be generally made from non-edible ligno-cellulosic biomass, including residues of crops or forestry production (corn cobs, rice husks, forest thinning, sawdust, etc.), and whole plant biomass (e.g., energy crops such as switch grass, poplar and other fast-growing trees and grasses). They include conversion of lignocellulose (woody or fibrous plant material) to a range of fuels including ethanol and synthetic diesel. Conventional first generation biofuels have been criticized for their high use of arable land, negative impacts on world food prices, biodiversity, limited energy yield, and sometimes poor lifecycle GHG emission reduction. Second generation technologies are being developed around the world to revolutionize the biofuel sector. Feedstock for second generation biofuels require advanced, capital-intensive processing to produce biofuels. But they promise to be more sustainable, offering higher emissions reductions and less sensitivity to fluctuations in feedstock costs [11]. However, technical advances in the production of advanced biofuels from cellulosic feedstock could make available a broader range of nonedible biomass (e.g. agriculture and forestry waste), which could ease feedstock supply and prices, and address certain sustainability issues [12]. For pure ligno-cellulosic biofuel plants to be economically competitive, they require a minimum size of around 200–1000 ML of yearly fuel production and respective large biomass supply [13]. The minimum resource need of a 200 ML, enzymatic ethanol plant is approximately 500 thousand ton (kt) [13]. Biomass production, on the other hand, is locally variable and has limited capacity, constrained by land use, soil, climate and nutrient supply. Energy content, spatial density and temporal variation are the primary influences on the security of biomass supply, harvest and transport costs and are thus key factors determining the viability of potential biofuel plant locations.

Feedstock costs account for 45–58% of the total production costs for second generation biofuels, depending on conversion efficiency and applied technology [14,15]. Transport of biomass to processing facilities is potentially an expensive component of energy or fuel production, therefore the spatial concentration of available biomass could be a limiting factor in the viability of facilities proposing to use locally produced feedstocks.

India is favorably situated regarding potential biomass energy resources than most countries, having around five times the world’s average amount of productive land per capital. India has a large land area of 7.69 million km2 . It is therefore seen by many around the world as potentially a large bio-energy and biofuel provider. In India, the in-field residue components of grain crops are commonly referred to as stubble.

Cellulosic biomass from current agricultural and forestry production systems (including biomass from hardwood plantations maturing by 2030) could produce 9.5 GL/ yr of ethanol, replacing 6.4 GL/ yr of gasoline, or 34% of current consumption. India has large areas of non-crop land that already produce grasses. At a conversion rate of 300 L of ethanol per ton of biomass, this would be sufficient to supply 12 GL or around 61.5 % of 19.5 GL petrol demand. Upper limits to production on estimates of second generation feedstock resources in India are shown in Figure 1.

Figure 1. Upper limits to production on estimates of second generation feedstock resources in India. (A-Ethanol from all feedstocks) (B- Ethanol from reasonable available fraction of feedstocks) [16]

For further evaluation and quantitative assessment of the availability of biomass, Remote Sensing and GIS (Geographical Information System) are two important techniques that can be employed [16]. Second generation biofuels provide a substantially more sustainable alternative as they are based on nonedible biomass sources, which do not compete with food and offer the potential to significantly lower the life-cycle GHG emissions compared to non-renewable alternatives which is an increasingly important requirement in a carbon-constrained world.

Second Generation technologies are still under development and not yet used widely for commercial biofuel production. They include the use of lignocellulosic plants as feedstock to manufacture ethanol, syngas, synthetic diesel, dimethyl ether and furans, as well as the production of algal lipids to convert to biodiesel.

Two major platforms exist for the conversion of lignocellulose to fuel: 1) Thermochemical–where lignocellulose is heated to a moderate or high temperatures to break down the structure of the polymers to smaller chemical mixtures which are subsequently converted into fuels by catalysts or micro-organisms, and 2) Enzymatic – where natural polymers of sugars found in cellulose and hemicellulose are broken down into individual units and then processed to fuels by fermentation with organisms such as yeast.

The relative cost hierarchy for biomass resources invariably places a higher price on their use for food, fiber and transport fuel. Changes in policy to address climate change are expected to increase the costs of petroleum based fuels therefore pushing the value of transport fuels higher. This may close the cost gap between transport fuels and food applications.

The majority of the second generation biofuels processing technologies are not yet available on a fully commercial scale, so the biofuels are expected to enter the market within a few years. There are many unexplored areas where innovative thinking could provide breakthrough conversion technologies to lower the cost of lingocellulose conversion.

India has a technologically-driven, modern agricultural sector that could benefit from the development of new regional industries based around non-food biofuel crops. Communities, particularly rural ones, have an opportunity to explore the options for growing energy crops on underutilized land [4]. Community benefits could also be gained from the creation of jobs from new industries. The implementation of biofuels into economies will be conditioned by several factors including local, global and national issues, types of feedstock or level of development of the market.

Commercial scale facilities can be considered to be an output of 25 million liters or more of biofuel per year [17]. The compliance certificates data of USA EPA (United States of America Environmental Protection Agency) suggest that no cellulosic biofuel was used before 2012 and about 0.00002 b.g. (20,000 gallons) were used in 2012 [18]. Six commercial-scale facilities are currently in construction and many more are planned in the near term [19]. A complete summary of biofuels demonstration and commercialization activity in the USA and in the EU presented by Balan, et al. [17] suggest that majority of the projects in the USA and the EU are either at pilot/demonstration scale or under advanced stages of construction of commercial plants. USA is planning the production of 60.5 BL of second-generation bioethanol by the year 2022. Biomass feedstock to meet Energy Independence and Security Act (EISA) advanced biofuels mandates are estimated to increase from 21 to 224 million dry Mg from 2012 to 2022 [20]. In February 2012, the USA Department of Energy (DOE) invested more than US$1 billion in 29 integrated projects to produce advanced biofuels, including ethanol, butanol, gasoline, diesel, jet fuels, chemicals and power. EU has announced a 10% target for replacing transport fuels with biofuels by 2020 [22].

In regards to ligno-cellulosic ethanol production programs, the European Commission supported seven industrial demonstration projects through the 7th Framework Program (7FP), for a total of more than €70 million [21]. The biomass resources in the EU may not be adequate for meeting the 2020 and 2030 EU biofuels targets and it may require a significant import of biomass feedstock from different parts of the world [21]. In China, although there is no commercial operation yet because of high production cost, there were eight pilot and demonstration plants in operation by December 2009 [23].

Several commercial-scales ligno-cellulosic to biofuel plants e.g. Iogen's planned enzymatic plant in Saskatchewan, Canada and Choren's thermochemical plant in Germany which are in the planning stage will be coming on-line soon. However, it is still difficult to obtain true capital and operating costs of commercial-scale production of biofuels from ligno-cellulose.

The production of second-generation biofuel in India is currently in its infancy and its production from sugar production wastes and agricultural biomass is currently in the development phase.

However, growing urgency to move away from a fossil-fuel economy is overshadowing the need to adopt a precautionary approach to biofuel development, which would consider potentially long-term and severe environmental threats presented by second generation feedstocks [24]. Clearly, potential environmental impacts of the emerging bioenergy sector carry little economic or political weight when compared with the immediate and pressing issues of energy security and climate change.

Obtaining biofuels from nonedible energy crops and the investigation of new energy crops as raw materials have been increasing both in the world biofuel sector and in scientific studies [25]. Commercial production of second generation biofuels will (i) solve agricultural residue disposal problem, (ii) reduce the cost of agricultural residue treatment, (iii) produce the alternative fuel (iv) reduces fire hazard (v) Stimulation of jobs and rural and regional development, (vi) provide local environmental benefits and (vii) help in carbon sequestration and carbon management.

The production of biofuel from ligno-cellulosic biomass on a commercial scale requires mature technology and experience. The production cost of ethanol depends strongly on the availability and characteristics of lignocellulosic biomass as well as the chosen production strategy. At the current state of technological knowledge, the main challenge faced by second generation biofuels are economic in nature. When compared on the basis of cost of production (excluding external costs to society), they are still simply too expensive to produce, relative to the fossil fuels that they are projected to replace [28]. Given the investments in research and development, economic theory would indicate that, under- investment from the private sector is likely. Policy interventions could help accelerate the transition from first generation to the commercial deployment and uptake of second generation biofuels. In EU, the tax incentives have contributed to directly boost biofuel consumption [29, 30].

Biofuel support policies are key drivers for the promotion of biofuels and have been adopted in several developed as well as developing and emerging countries [31]. However, these countries are not yet directly addressing second-generation biofuels in their policies. One of the main drivers for second-generation biofuel production in the next years will be a steadily increasing blending mandate for cellulosic ethanol. The USA focused on the development of second-generation technologies and has set significant production targets from cellulosic sources. It still remains unclear how much support will be needed before the biofuel industry will be independent of governmental support [28].

Feedstock trade with countries that currently cannot provide suitable framework conditions for a domestic second-generation biofuel industry could be an option for ensuring sustainable supply of feedstock. This might only bring limited economic benefits, but could be a possibility for less-developed countries to profit from the growing demand for second generation biofuels globally.

In India, the production of second-generation biofuel from agricultural residue is currently in the development phase. Recent studies suggest that, crops grown specifically for energy supply purposes have less immediate potential for using energy than existing crop residues because of the higher delivered costs in terms of $/GJ of available energy [32]. Under the current conditions of zero fuel excise and oil prices around US$ 80 per barrel, ethanol production is viable using biomass with a plant gate cost of up to US$ 69.60 per ton [11, 12]. In transport, a mix of several alternative fuels will be needed to replace oil, with specific requirements of the different modes. Biofuels will probably be a main option for aviation, long-distance road transport, and rail where it cannot be electrified. Work to ensure sustainability (e.g. on indirect land-use change) is on-going. The market uptake of new bio-energy which reduces the demand for the land necessary for food production and which increases the net GHG savings (e.g. biofuels based on waste, algae, forest residues) should continue to be promoted. There is a need to invest in second and third generation biofuels. As technologies mature, costs will decrease and financial support can be reduced. While significant cost reductions are needed for second generation biofuels, the present policy instruments, such as fiscal incentives and consumption mandates have in general, not differentiated between the first and second generation biofuels. The policy regime should be revised to account for the relative merits of different types of biofuels.

From the study, it is recommended that, there are great opportunities for the production of second generation biofuels in India.

In India, the production of second-generation biofuel is currently in its infancy and its production from sugar processing wastes and agricultural biomass is currently in the development phase. This paper provided an overview of the second generation biofuels in an Indian context and described the barriers to wider adoption of those biofuels. India has a large land area and an advanced agricultural industry. It is therefore seen as a potentially large bio-energy and biofuel provider. This review explained the development of second generation biofuels industry in India, summarizing the approximate costs for commercial scale plants from the literature along with major commercial and research programs in second generation fuels production in the country. There is a need to invest in second and third generation biofuels in India because as technologies mature, costs will decrease and financial support can be reduced. India has a technologically-driven, modern agricultural sector that could benefit from the development of new regional industries based around non-food biofuel crops. Communities, particularly rural ones, have an opportunity to explore the options for growing energy crops on underutilized land.